Creating Passive Income

Showing busy people how to add cash flow to their investment portfolio

Because It’s Time To Seek Real Estate Investing Advice From Experts

If you want to invest in real estate but aren't excited about doing all of the work, you're in the right place.

How It Works

The Cash Flow Savvy System™

The Cash Flow Savvy System™ is a game-changer for those looking to create passive income through real estate at an accelerated rate. Designed specifically for the average person, this system empowers you to achieve financial freedom and provides peace of mind for your financial future.

With our proven passive income system, you'll be able to break free from the old financial rules and create a life of options. You can say goodbye to financial worries and hello to more free time, all while accelerating your journey towards exiting the "rat race."

Investors who have implemented The Cash Flow Savvy System™ have been able to exit the rat race ten times faster than those following traditional methods. Don't wait any longer to take control of your financial future - start building your passive income today with The Cash Flow Savvy System™.

The Cash Flow Savvy System™

Accelerate Your Path to Financial Freedom with The Cash Flow Savvy System™: The Ultimate Game-Changer for Passive Income through Real Estate

Escape the Rat Race

Say goodbye to financial worries and hello to more free time as you accelerate your journey towards exiting the "rat race."

Implement the Proven System

Investors who implement The Cash Flow Savvy System™ can exit the "rat race" ten times faster than those using traditional methods.

Master Passive Income

Take control of your financial future and start building your passive income today with The Cash Flow Savvy System™.

Unlocking the Secret Formula for Success

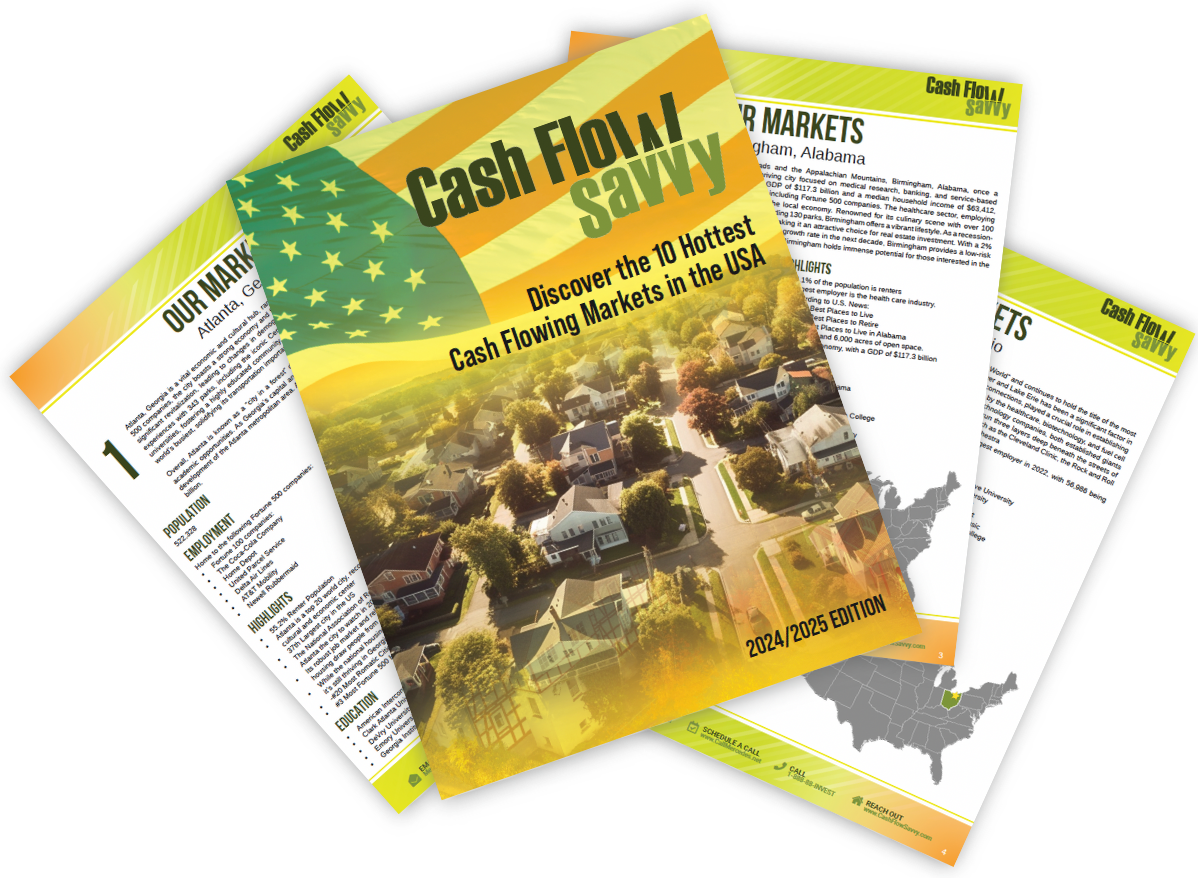

Discover the Ultimate Passive Income Strategy with the Top 10 Cash Flow Markets in the USA

No Compromise, Just Maximize.

Because It’s Time To Seek Real Estate Investment Advice From Experts

100%

Satisfaction Guaranteed

243M

Acquired Real Estate

250+

Raving Fans

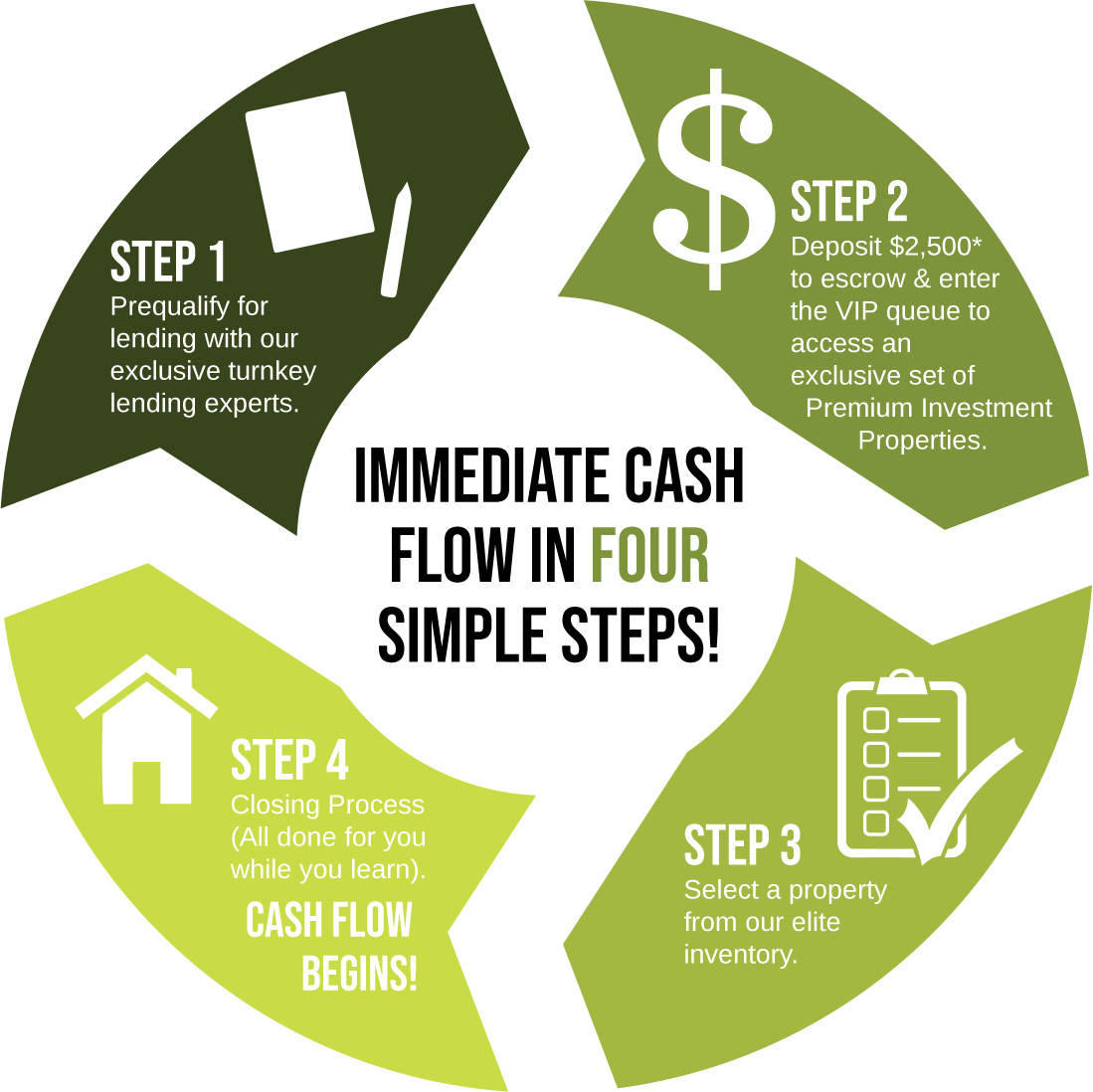

We find the property, buy it, rehab it, find tenants, manage it.

Then we collect rent and send it to you.

You buy the property from us WITH CASH FLOW!

Hear What Our Cash-Flowing Raving Fans Say

Our mission is to empower you to generate passive income through real estate faster than you ever thought possible. With our help, you can secure your financial future and enjoy the peace of mind that comes with a steady stream of passive income.

Phillip Mutulo

"I wanted to make sure my first purchase was going to be a solid investment and I knew help would be needed. The support I received during the process was outstanding! They held my hand every step of the way and I guided me through the entire process. I was blown away with my experience and have referred my friends as a result."

Jennifer Omhari

"I honestly couldn't have bought my property without Mercedes and the CashFlow Savvy Team. They literally held this newbie’s hand throughout the entire process and believe me, I needed a lot of hand holding. If it wasn't for them, I would still be wishing I was a real estate investor right now instead of actually being a real estate investor. How do you thank someone in words for all of that? It's just not possible. Nothing seems adequate."

Nate Hammond

"I found CashFlow Savvy after listening to Matt's Turnkey Real Estate Investing Podcast on iTunes. At the time I was in the market for a turnkey provider for my first property. After my consultation call with Mercedes, I felt confident that CashFlow Savvy was the right choice for me! Right away Mercedes started sending me available turnkey properties. Once I found the right one for me the CashFlow Savvy essentially took care of the rest! Throughout the process, the CashFlow Savvy team was both responsive and proactive in answering all my questions and guiding me through the process of buying my first investment property."

Ray Rosato

"I met the CashFlow Savvy team at a property tour and instantly knew they were the right choice for me. I found Mercedes and the team to be very accessible, experienced, and relationship-oriented. They are very selective in qualifying properties and look out for your interest. They also provide great contacts and tips which helped facilitate a smooth transaction during this first purchase."

Lori and Carlos

"Working with Mercedes and the team at CashFlow Savvy was a breeze. We're on our way to becoming financially free and I wish we had done this sooner!"

Enrique & Irem Santana

"From our first conversation to our latest transaction, Mercedes and the team she’s connected us with have been extremely helpful and essential toward making our financial goals a reality. At the beginning of the year, we had a savings account with a nice pile of cash doing nothing for us and no investment properties. Today we don’t have much in our savings but have 6 cash flowing rentals which cover over 1/3 of our expenses. It’s nice to have a team that can answer any questions we may have and is ready with quality cash flowing investment properties every time we are ready for one."

Lanita Holland

"Being able to work with a company that has experience with their own personal investments as well as experience with helping others find investments for themselves has been very valuable. The team at CashFlow Savvy, as well as the teams they have in the cities they work in, were patient, helpful and always willing to share their knowledge when I needed it.

To date I have purchased 2 properties with CashFlow Savvy and I plan on purchasing many more in the future. They make the process as easy as possible. The hardest part was raising the capital! Thank you for giving me a truly Turn Key experience."

Seth Leiboh

"I can't believe acquiring my first rental was so easy!"

Get In Touch

Email

Mercedes@CashFlowSavvy.com

Address

11035 Lavender Hill Dr

Suite 160-159

Las Vegas, NV 89135

Assistance Hours

Mon – Sat 9:00am – 5:00pm PST

Sunday – CLOSED

Phone Number

1-888-88-INVEST

Let's Connect

Let's become friends! What are you waiting for?